Home /

Expert Answers /

Finance /

given-the-monthly-returns-that-follow-find-the-mathrm-r-2-alpha-and-beta-of-the-portf-pa699

(Solved): Given the monthly returns that follow, find the \( \mathrm{R}^{2} \), alpha, and beta of the portf ...

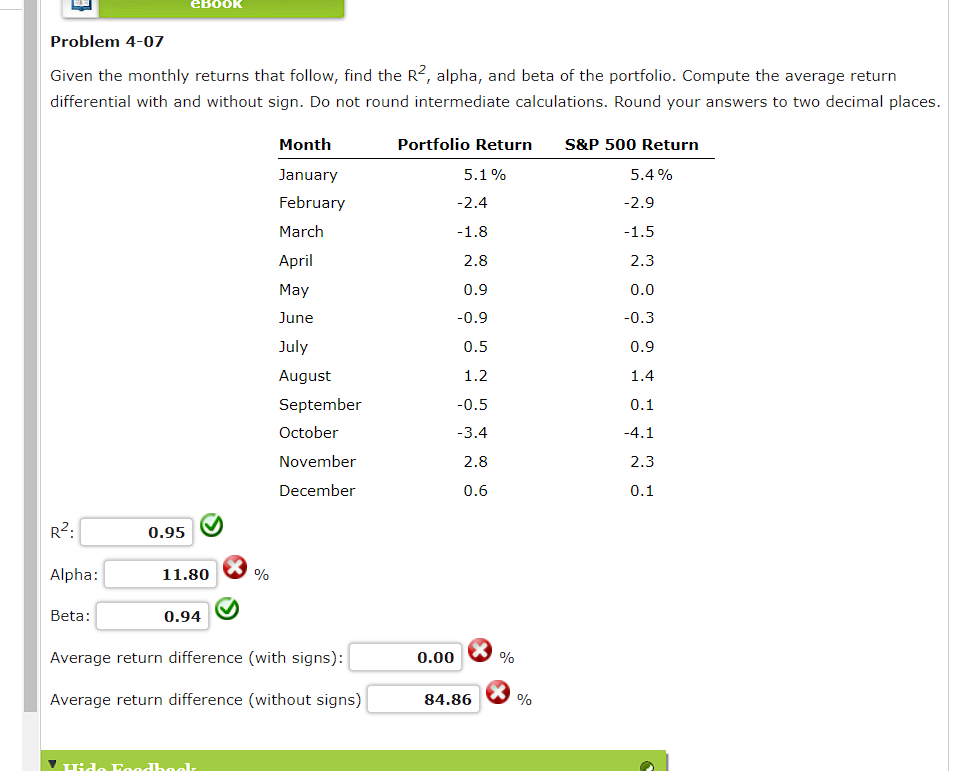

Given the monthly returns that follow, find the \( \mathrm{R}^{2} \), alpha, and beta of the portfolio. Compute the average return differential with and without sign. Do not round intermediate calculations. Round your answers to two decimal places. \( \mathrm{R}^{2}: \) Alpha: \( 3 \% \) Beta: Average return difference (with signs): \( 8 \% \) Average return difference (without signs)

Expert Answer

EXCEL: Month Portfolio return S&P 500 return Difference with signs Difference without signs January 5.1% 5.4% 4.7%